Unraveling the Power of Equipment Financing: A Comprehensive Guide

As the engine of a successful business continues to roar, understanding the facets of commercial equipment financing is critical for both seasoned business owners and aspiring entrepreneurs. One integral element that stands out in this arena is equipment financing, a unique and flexible financial tool that can propel businesses to new heights.

What is Financing?

It’s providing funds for business activities, making purchases, or investing. Financial institutions such as banks, credit unions, and finance companies provide these funds, which may come in the form of loans, leases, or hybrid loans known as Equipment Finance Agreements (EFAs).

Commercial vs. Personal

There’s a significant distinction between commercial and personal financing. Personal involves managing personal monetary affairs, including saving, investing, and budgeting for individual or family needs. It usually revolves around acquiring personal assets like homes, cars, or funding personal expenses or investments.

On the other hand, commercial is the allocation of loans and other forms of financial support to businesses. It covers an array of financing types, such as equipment, commercial real estate loans, business lines of credit, and more. Commercial finance focuses on bolstering a business’s operations, growth, or asset acquisition.

A Valuable Business Tool

Equipment financing, our prime focus, is a powerful commercial financing method that enables businesses to purchase or lease the equipment they need without shelling out substantial upfront costs. This method offers a way to secure advanced machinery, technology, or other business-essential equipment while preserving cash flow.

Benefits of Equipment Financing versus Cash

- Cash Flow Conservation: By financing equipment, businesses can preserve their cash for other crucial operations or unexpected expenses.

- Up-to-Date Equipment: Given the pace of technological advancement, equipment can become obsolete quickly. Financing provides the flexibility to upgrade as needed.

- Tax Advantages: Under Section 179 of the IRS Tax Code, businesses can deduct the full purchase price of qualifying financed or leased equipment in the acquisition year.

- Easier Budgeting: financing involves fixed monthly payments, helping businesses plan and manage budgets effectively.Check out more benefits here

Countering Common Misconceptions about Financing

Despite its numerous benefits, some misconceptions might deter businesses from considering equipment financing.

- Misconception: Financing is too expensive. Contrarily, with competitive interest rates and potential tax benefits, equipment financing can often be more cost-effective than upfront cash purchases.

- Misconception: My business won’t qualify. Many businesses, including startups and those with less-than-perfect credit, can qualify for equipment financing. Lenders consider various factors, not just credit scores.

- Misconception: The application process is complicated. While some financial tools can involve complex procedures, many lenders streamline their processes to provide swift and straightforward financing solutions.

In a competitive business landscape, effective financial management is key to sustainability and growth. Through financing, businesses can unlock potential, harnessing the power of advanced equipment while maintaining robust financial health. Don’t let misconceptions hold back your business’s growth—explore the possibilities that financing can offer today.

If you’re interested in learning more, we are always happy to chat with you; or you’re welcome explore our website and other blog topics. Ready to purchase? Fill out our no-obligation application!

Keywords: Equipment Financing, Commercial Financing, Personal Financing, Loans, Leases, Equipment Finance Agreements (EFAs)

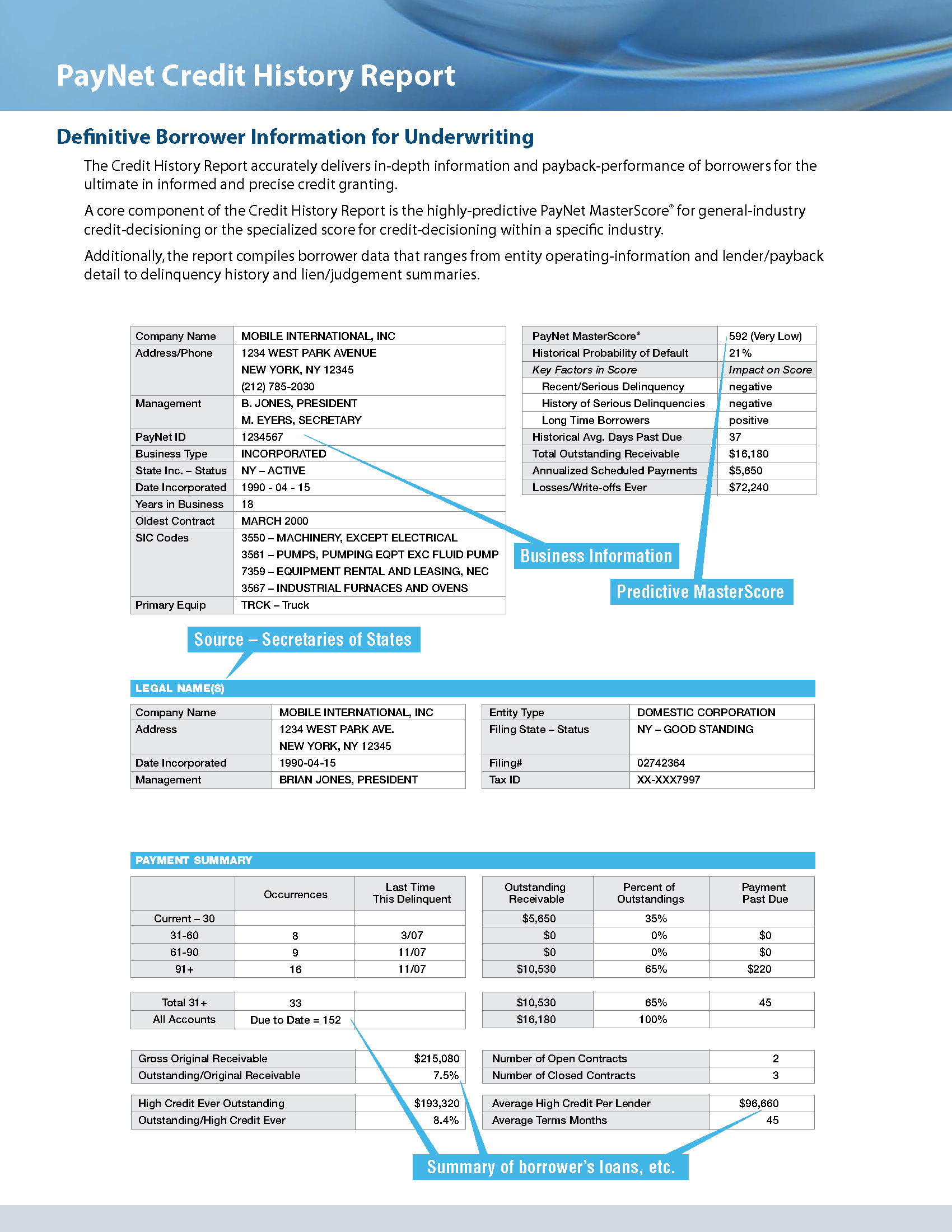

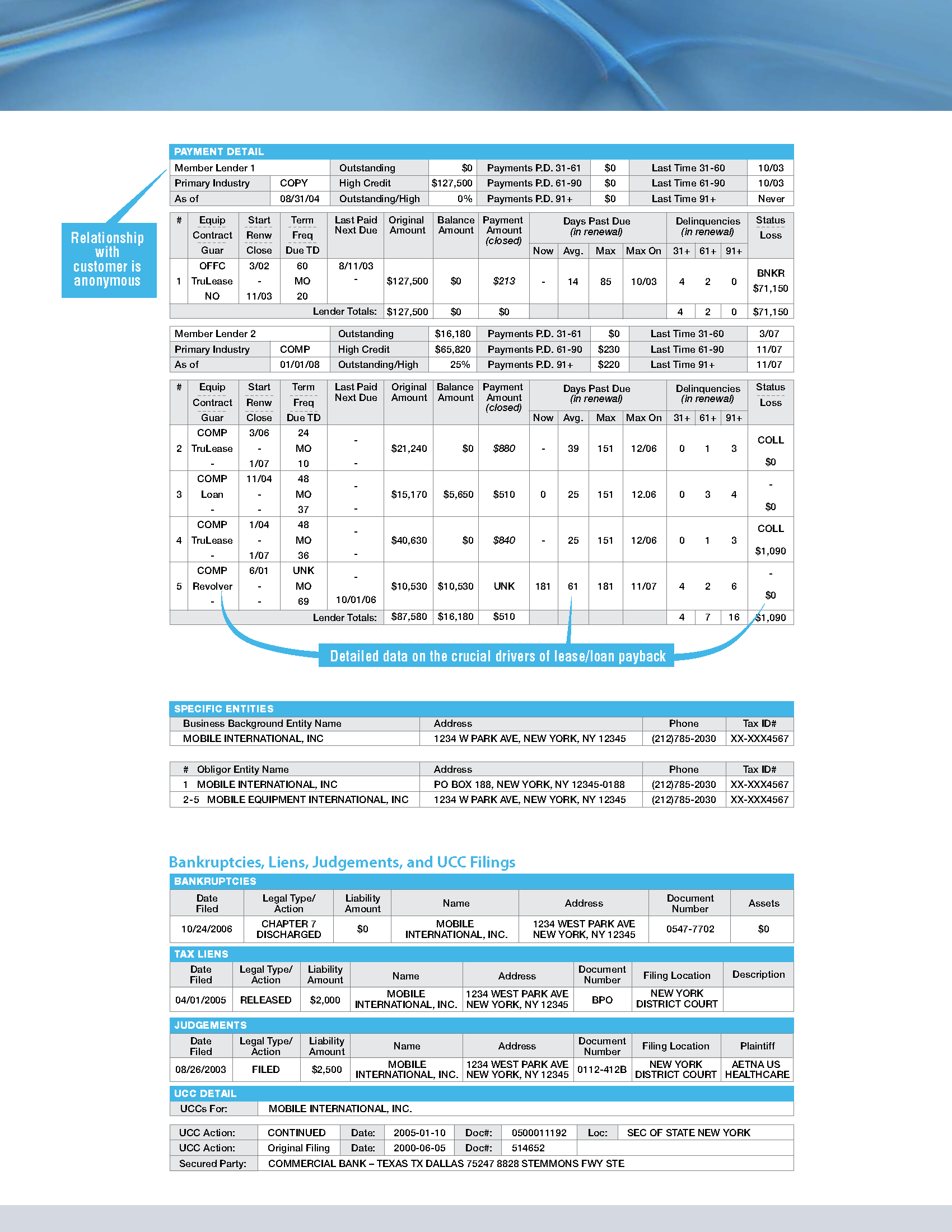

Step 1. Know what’s in your credit profile!

Step 1. Know what’s in your credit profile! Financing comes down to two things. First: How likely is the lender to get their money back? And second, What’s that risk worth to the lender. That’s it; when you strip away all the complexities and jargon…that’s financing in its simplest form. Now, as we add in variables to the risk like: credit profile, industry type, equipment type, time in business, amount requested, etc. things get more complicated and complex. However, from these added variables we are able to more accurately quantify risk and access whether someone is qualified to pay back what they borrow. If the lender is able to mitigate the risk, then they’re better able to get their money back.

Financing comes down to two things. First: How likely is the lender to get their money back? And second, What’s that risk worth to the lender. That’s it; when you strip away all the complexities and jargon…that’s financing in its simplest form. Now, as we add in variables to the risk like: credit profile, industry type, equipment type, time in business, amount requested, etc. things get more complicated and complex. However, from these added variables we are able to more accurately quantify risk and access whether someone is qualified to pay back what they borrow. If the lender is able to mitigate the risk, then they’re better able to get their money back.

Step 4. Don’t throw it out!

Step 4. Don’t throw it out!