Business Credit: A Free Summary

If you read the title and thought, “Whoa buddy, I didn’t even know my FICO score two minutes ago. Now you’re telling me my business has credit I have to manage too?!”, then relax; it isn’t that bad. It is however a little bit of work on your part, but you’re a business owner and you’re used to work.

What is Business Credit?

Business credit is not too much different than personal credit in that it is a compilation of the times you’ve borrowed money and how well you did managing that debt. Personal credit is attached to…well…you. Business credit is attached to your business. If you need to sit down after reading that, go ahead and take a few; otherwise we’ll just roll right along.

Your business credit can be affected by a number of things from tax liens, to late payments on credit cards, to defaults on loans or lines of credit. Even paying late once can cause your score to dip drastically. So make sure you stay on top of those payments as best you can!

Keep in mind that, like your personal credit score, your business profile will see small ups and downs depending on how much you’ve paid off, if you’ve added credit or had a hard inquiry. Don’t worry too much about small fluctuations, they happen.

Who looks at Business Credit?

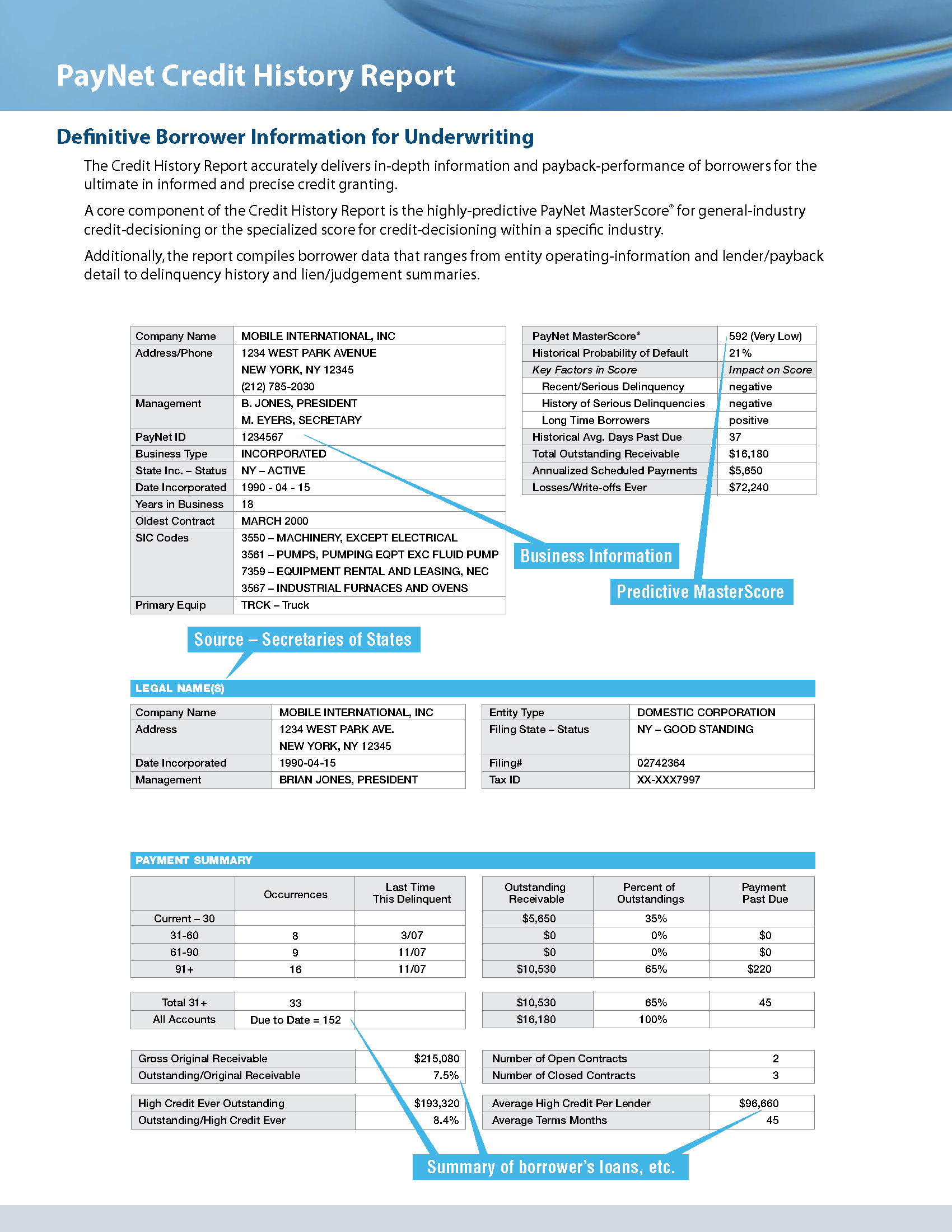

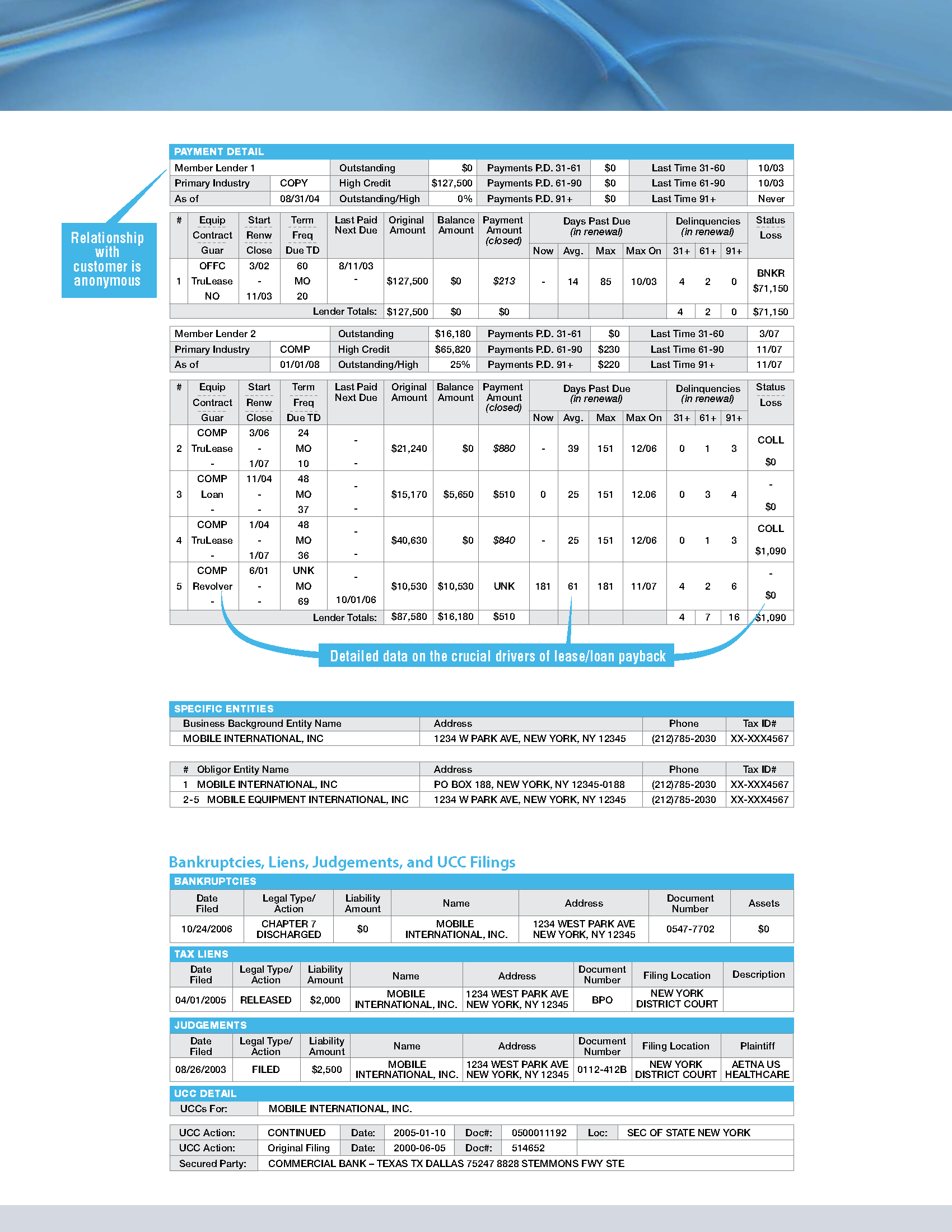

You should know that personal credit is reported to three major credit bureaus; Experian, Equifax, and Transunion (If you didn’t, checkout our personal credit post). Similar to personal credit, business credit is reported to three major credit bureaus. There is the one you’ve heard of: Experian; but also ones you may not have heard of like Paynet or Dun & Bradstreet. Mainly, in the equipment finance world, most lenders are looking for your Paynet score if they ask about the business credit. Paynet, for those of you who do not know, is owned by Equifax.

If you have never seen your business’s credit report, I would highly recommend requesting a copy of it. Just like with personal credit, there is always a potential for erroneous or fraudulent reporting. Unfortunately, business credit reports aren’t typically given out for free, but there are a number of sites that can pull all three simultaneously. At the time of writing this, Credit.net would give you a single limited report if you sign up for a free account/trial.

Why does Business Credit matter?

Well for one, the better the profile, the higher the odds of being approved. Who would you rather lend money to? The person who’s paid on time every time? Or the person who is constantly late or even worse stops paying completely? Pretty easy decision, you’d go with the safest option all the way down to the least safe. Lenders work the same way. They want the person most likely to pay on time and in full.

Secondly, it could save you thousands! The riskier you are considered to Lenders, the more they are going to charge you to borrow their money. Everything about you has a level of risk that Lenders look at when considering you for finance. They look at the industry you’re in and the type of equipment you’re buying, as well as credit profile. Having good business credit makes one less thing Lenders have to worry about when lending to you.

Thirdly, with strong business credit you can skip personally guaranteeing a transaction. That’s right, with strong business credit lenders will allow the company to take on the liability rather than you (the owner). Corp Only transactions are typically much more difficult to qualify for so taking care of the business’s profile is important.

Plan for the future!

“But I don’t plan on financing anything right now, why should I care?”, and to that I would ask, “Do you have road side assistance or towing for your car or truck?”…yea, you probably didn’t plan on getting in an accident the day you signed up for, but you had the foresight to see that one day you might need it; Similar principle here.

Maybe your equipment is newer or you think you’ll be flush with cash when you want to replace or add equipment to your arsenal…but new equipment breaks, businesses slow down, and that cash pile you thought you could hang onto is like sand in-between your fingers. Point is, life happens and what you thought might happen then might not be the case now.

Step 1. Know what’s in your credit profile!

Step 1. Know what’s in your credit profile! Financing comes down to two things. First: How likely is the lender to get their money back? And second, What’s that risk worth to the lender. That’s it; when you strip away all the complexities and jargon…that’s financing in its simplest form. Now, as we add in variables to the risk like: credit profile, industry type, equipment type, time in business, amount requested, etc. things get more complicated and complex. However, from these added variables we are able to more accurately quantify risk and access whether someone is qualified to pay back what they borrow. If the lender is able to mitigate the risk, then they’re better able to get their money back.

Financing comes down to two things. First: How likely is the lender to get their money back? And second, What’s that risk worth to the lender. That’s it; when you strip away all the complexities and jargon…that’s financing in its simplest form. Now, as we add in variables to the risk like: credit profile, industry type, equipment type, time in business, amount requested, etc. things get more complicated and complex. However, from these added variables we are able to more accurately quantify risk and access whether someone is qualified to pay back what they borrow. If the lender is able to mitigate the risk, then they’re better able to get their money back.

Step 4. Don’t throw it out!

Step 4. Don’t throw it out!